Alternative Insight

CONFUSION ABOUT TAXES AND DEFICITS - The real debt bomb

From the ups and downs of the United States' economy, policy makers seem confused in the functioning of the system they are trying to smoothly regulate, not considering that the economy has been created by distortions - government and private debt. Correcting the distortions is the route to correcting the economic decline. This is not happening.After several decades of government deficit spending and private non-initiatives, the United States has barely recovered from the economic collapse of 2008. The government's economic advisors have not resolved what caused the difficulties - a worthwhile objective to prevent future calamities - nor been able to institute policies for rapid recovery. Instead, anticipated expiration of the Bush tax cuts and planned spending cuts under the Budget Control Act of 2011have invigorated a debate on effects of tax hikes to the economy. In this debate Republican leaders cite authorities who claim that expiration of the Bush tax measures will result in the loss of 750,000 jobs, and the Congressional Budget Office (CBO) analysis predicts a slight recession with a lowering of the future budget deficit. Analysis demonstrates that the government has choices; added revenue can either be used to increase employment, prevent the debt from increasing, or attend to increases in entitlements. No reason for job losses. Lowering budget deficits is a gamble, depending upon investors redirecting their purchases of government securities to investments in private initiatives. The gamble must have an acceptable pay in order to prevent a recession.

Start with what determines the GDP:

Consumer Spending + Government Spending + Investment + Current Account = GDP

If Current Account is negative, which it has been for decades, then it reduces the GDP.

Using the equation, we note:

If the government has ample reason to increase the budget, spending on goods and services with the increased revenue from higher income and payroll taxes will compensate for any loss in private spending resulting from less after tax income. Because the eventual spending for goods and services remains the same as before the tax increases, the contributions to the GDP remain the sameWhere will the government spend the additional revenue? The Congressional Budget Office (CBO) has described a need for higher taxes.

What Factors Are Putting Increasing Pressure on the Budget?

The aging of the baby-boom generation portends a significant and sustained increase in coming years in the share of the population that will receive benefits from Social Security and Medicare and long-term care services financed through Medicaid. Moreover, per capita spending on health care is likely to continue to grow faster than per capita spending on other goods and services for many years. Without significant changes in the laws governing Social Security, Medicare, and Medicaid, those factors will boost federal outlays as a percentage of GDP well above the average of the past four decades-a conclusion that applies under any plausible assumptions about future trends in demographics, economic conditions, and health care costs.

CBO Choices for Deficit Reduction - November 2012The government can also spend the raised taxes for job creation. Because the present economic environment is not creating sufficient jobs, the added government revenue can be directly applied to do the task. Obvious examples, stated for representation, and which have already been performed are (1) Contracting new projects that require new employment, and (2) direct transfer of funds to states and counties to re-employ discharged workers. As employment increases, unemployment compensation decreases, a regenerative benefit to adding new jobs. Tax increases can redistribute wealth and, in times of economic stagnation and static investment, be an alternative route to job creation. Deficits have served this purpose, and an income tax increase can substitute for the deficit intention.

Evidently, there is confusion between lowering the government debt and lowering the budget deficit. Added tax revenue can be used to lower the debt without causing a drop in the GDP - repurchase of debt compensates for loss of private spending by transferring the tax revenue to investors, who may either reinvest or spend. This could be counterproductive. Uncertainty of reinvestment is one reason for the deficit - investors are not lending to the private sector.

If the budget deficit is decreased, regardless of whether tax rates are raised, lowered or remained constant, the decreased government spending will not affect the GDP if an equal amount of investment is transferred from deficit spending to support private initiatives. Present experience creates doubts this will happen. Investors prefer low interest rate government bills and bonds to higher rate investments in the private sector. Let the government take the money and invest in the economy. Besides, due to the causes of budget deficits, for which the government is not responsible, budget deficit reduction is not a simple task. More on this later.

Summarizing - With all other economic factors, including interest rates, constant,

(1) income and payroll tax increases don't change system money supply or purchasing power and just shift them around. If the added revenue pushes the federal budget higher, then the tax increase should not effect GDP or employment;

(2) although not desirable, government debt can be lowered by using tax increases to retire debt without negatively affecting the economy with one caveat - the credit must be recirculated in the economy;

(3) similarly, with a caveat, budget deficits can be decreased without affecting the economy - intended, but not fulfilled investments in government securities must be used for private investments. Present history indicates that this will not happen and the economy will suffer if the deficit spending decreases. The impulses for deficit spending will not go away, and deficits will not be easily reduced. Examination of the strong economy during the Clinton era, when budget surpluses occurred and the economy advanced, will demonstrate how investment factors compensated for the impact of the advance to budget surpluses.Implementing the other half of the Budget Control Act of 2011 - reducing government spending - will have a drastic effect on the economy. The equation above illustrates this admonishment. Reduce government spending by one dollar and the GDP will be reduced by one dollar - well, not quite; the current account deficit may also be reduced (less foreign purchases) and investors may find other opportunities with their money than purchasing government notes and bonds. On the other hand , it could be more drastic than one for one - increased unemployment means less government revenue, which means aditional federal spending cuts. More balanced budgets also portend a stronger dollar, which leads to reduced exports and increased imports, and a rise in the current account deficit.

The most important of the possible spending cuts is the defense budget, Despite its waste, tendency toward earmarks, and contracts for production of non-productive hardware that use massive resources, the aerospace and defense industries have become a necessity, not for national defense but for national economic survival. The consulting firm Deloitte, in a study The Aerospace and Defense Industry in the U.S. A financial and economic impact study, March 2012 estimates

the grand total direct, indirect and induced employment associated with the U.S. aerospace and defense industry is 3.53 million jobs, not including industry skilled workers employed by the Federal government or airlines.

We estimate that these U.S. aerospace and defense companies generated $324.0 billion in sales revenue in 2010, with $15.6 billion in net income after tax at an average pre-tax reported operating profit margin of 10.5%. This margin percent metric was below average, when compared to other industries in America. These companies paid $5.5 billion in corporate income taxes on their earnings, as well as $1.7 billion in state income and similar business taxes. Thus together with individual direct employee taxes, the total industry generated an estimated $37.8 billion in wage and income based taxes to state and Federal government treasuries, not including the taxes paid by indirect and induced industry employment.

The role of the defense department in providing sustenance to the free enterprise system is not well presented. Entire industries - defense, armaments, electronics, ship building, aviation, space exploration - and parts of some industries - airlines, plastics, chemical, metallurgical, Internet - owe their existence and prosperity to developments, funds and contracts from the defense department. As the leading arms exporter, an outgrowth of defense procurements, the U.S. lowers its trade deficit and brings purchasing power into the nation. Without the arguments and preparations for war, the free enterprise economy would have been shaky decades ago. Its weapons of war are only an undesirable feature that must be accepted in order to have other benefits. Unfortunately, any demise of the defense industry will cause a decline in the other industries. Unless the existing military budget can be transformed into an equivalent civilian budget, the U.S. is stuck with its defense industry.

And unless the policy makers understand the reasons for the deficit, the U.S. will be stuck with continuous deficits. Four factors augment the federal deficit.

(1) When private debt, which has driven the economy since 1982, falls, government debt must rise to maintain the economy in balance and enable it to continue growing.

(2) The deficit in the current account, triggered by a negative balance of payments, circulates back as debt. The government is forced to issue sovereign debt in order to repatriate the money and regain purchasing power in the system,

(3) If profit is not reinvested, the economy will fall. Enter government deficits to offset lack of reinvestment.

(4) Purchasing power is sidetracked to speculation and remains outside the merchandise economy. Government again to the rescue to increase purchasing power and demand.

Unless these factors are positively readjusted, the government budget will suffer major deficits. Because the tax arrangements don't entirely affect these factors, they will not greatly affect the deficit. If these contributions to the deficits decrease, they will be due to a decrease in imports - mainly petroleum - or to an increase in either exports, private debt or private investment.By inaccurately estimating how taxes affect the economy, and by neglecting to contemplate all the factors affecting the federal deficit, policy makers have diverted the course of economic recovery. Adjusting parameters without understanding that the parameters are the result of system problems and not their cause has led to stagnation. Shibboleths, such as raising taxes will lower spending and cut 750,000 jobs and raising taxes will greatly decrease the deficit are mistakes. Moving figures around will not solve the nation's economic problems. Policies must start with understanding of the deficiencies that lead to economic downfall.

(1) For a capitalist economy to survive, profits must be quickly and constantly reinvested in the domestic economy and not overseas.

(2) The economy is driven by debt, which will periodically saturate.

(3) A negative current account sucks purchasing power out of the economy and leaves production without demand.

(4) Financial speculation circulates money out of the domestic economy and also provides a mismatch between supply and demand, or in effect, lowers demand and then supply.

(5) Capital demand for high profit speculative transactions lowers capital availability for domestic production.A series of charts bring these statements into perspective.

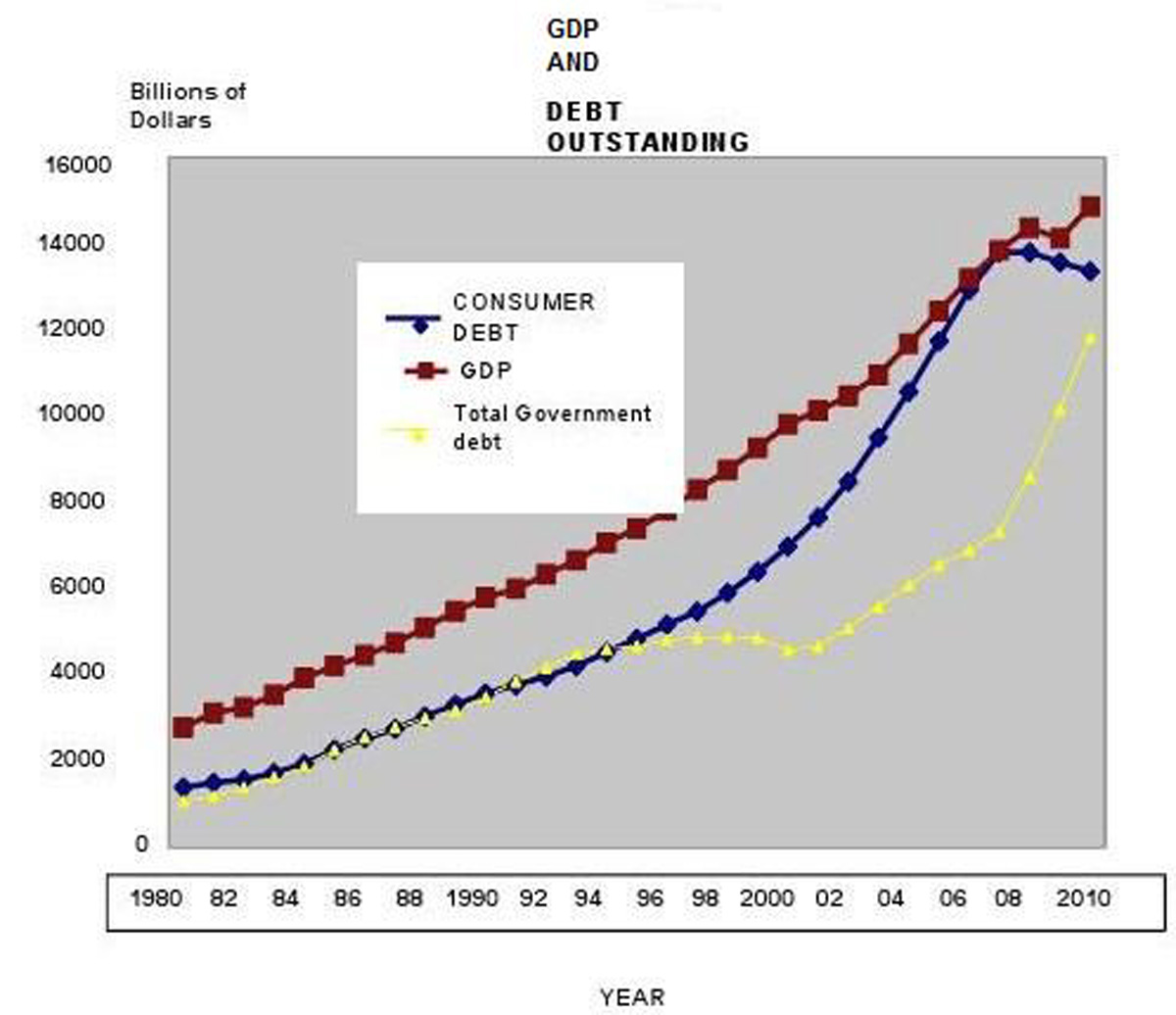

The chart below shows that when private debt increases abruptly, government debt stagnates or increases slowly and vice-versa; during deleveraging, government deficits increase. It also shows that debt drives the GDP.

The rapid increase in private debt during the Clinton presidency more than compensated for the lowering of the budget deficit and eventual budget surpluses. Notice the upward change in the slope of consumer debt during the years 1993, 1998, and 2001. Clinton's administration, either from chance or deliberation, took advantage of the impulse to the economy by the private sector debt to reduce the contribution from the government sector.

The next chart explains why federal deficits did not always drop greatly during rapid increases in private debt. Years in which the current account deficit increased (2007-2009) were also years in which government deficits were incurred. Sale of government securities to foreign nations offset the current account deficit. When consumer borrowing fell, imports also fell and the current account deficit decreased. Nevertheless, severe consumer deleveraging, shown in the previous figure, triggered government deficits. Without excessive government deficits, the GDP would have gone into free fall.

Another significant factor in the debt problem is the financial sector - possibly the most troublesome. The chart of US Debt by Sector shows the rapid growth of financial sector debt since the Reagan administration, $600 billion to $15 trillion, creating a shadow banking system, and sidetracking money supply into speculation and revolving investment, which deprives the merchandise economy of needed demand.

What does all this show? Simply, that resolving the nation's economic and unemployment problems has little to do with the tax schedule and erratic government spending. Solving the problems starts with facing the truth, which is that the private economy has caused its own problems. What needs to be done?

(1) Turn the economy away from being overly credit driven. This means slower and more even growth.

(2) Stimulate manufacturing industries to compete with imports (energy) and enable those that can export. Government is forced to subsidize industries and those industries can be mundane.

(3) Force corporations to rapidly reinvest profits in the USA. Tax unused profits.

(4) Legislate away rampant financial speculation. Laws are available to accomplish that purpose.

(5) Re-distribute wealth. The private sector cannot create sufficient jobs without redistribution of the wealth. One executive who reduces compensation from $5 million/yr to $500 thousand/yr can hire about 45 more employees. He/she will live well and others won't starve.Solving the debt problem is more pernicious. The government debt held by the public can be slowly canceled by replacing debt rollover with added taxes - another redistribution of the wealth - and by inflation. The almost 50% of federal debt that is not owed among government agencies but held by foreign sources, $4.5 trillion in 2012, can only be lessened by a positive current account. Any direct repurchase of debt is an import, and, as the equation shows, will lower the GDP. Can the current account be made positive? If so, when? Not in a far future. This is the real "debt bomb," and no amount of taxes will solve this problem. Only a miracle in recovery of export driven manufacturing can do the task - a highly unlikely venture. The much disparaged government, the Green Hulk of the non-comic world, will be forced to do the job. Get ready for a little statism.

Added notes, which illuminate the debate on halting a trip over the fiscal cliff.

(1) Although an increase in taxes will not affect the GDP, the Republicans principal thrust has been to insist on having Bush era taxes remain constant. A cut in federal spending will cause a reduction in GDP and predictions of 2-3 million job losses. The GOP leaders welcome that catastrophe. (2) The intention of the Stimulus Plan was to heighten demand. What limited the demand? The slow growth in private investment (credit) and reduction in domestic purchasing power due to the current account deficit are the principal culprits. Despite this awareness, neither of these problems are directly attacked. (3) Conservative economists complain that government deficits crowd out private investment. However, investors are satisfied to purchase low yield government securities rather than engage in higher yield investment opportunities. The government deficits are due to the lack of backbone from the financial sector, which evidently has no faith in its own economy.

alternativeinsight

december, 2012HOME PAGE MAIN PAGE

alternativeinsight@earthlink.net

No Need to Login to post a comment.

comments powered by Disqus